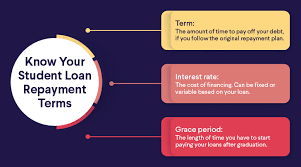

Student debt can feel overwhelming, but with proper planning and disciplined financial habits, it can be managed effectively. The first step is understanding how much you owe, including the total loan amount, interest rates, and repayment deadlines. Knowing these details helps you make smarter decisions and avoid financial stress in the future.

Create a Realistic Repayment Plan

A well-organized repayment plan is essential for managing student loans. Start by calculating your monthly income and expenses, then decide how much you can comfortably pay toward your loan each month. Paying more than the minimum amount whenever possible can reduce your interest burden and help you clear the debt faster.

Focus on High-Interest Loans First

If you have multiple loans, prioritize the ones with the highest interest rates. This strategy, often called the “avalanche method,” helps reduce the total interest paid over time. Continue making minimum payments on all other loans while directing extra money toward the most expensive loan.

Avoid Missing Payments

Late or missed payments can damage your credit score and increase financial pressure due to penalties and extra interest charges. Setting up automatic payments or reminders can help ensure that you never miss a due date. Consistent repayment also improves your financial reputation for future borrowing.

Build a Budget and Control Spending

Managing student debt becomes easier when you follow a monthly budget. Track your spending habits and reduce unnecessary expenses such as excessive shopping, entertainment, or eating out frequently. Saving even a small amount each month can help you make extra loan payments and reduce debt faster.

Increase Your Income Sources

Finding additional income sources can speed up your loan repayment journey. Part-time jobs, freelancing, tutoring, or online work can provide extra money that can be directly used to pay off student loans. Using bonuses or extra earnings wisely can significantly shorten the repayment period.

Consider Refinancing Carefully

Loan refinancing may help lower your interest rate and monthly payments, especially for private loans. However, before refinancing, compare different lenders and understand all terms carefully. Refinancing federal loans may remove certain government benefits, so it is important to evaluate the pros and cons first.

Maintain an Emergency Fund

While paying off debt is important, keeping a small emergency fund is equally necessary. Unexpected expenses like medical bills or job loss can create financial problems if you do not have savings. An emergency fund prevents you from taking additional loans during difficult situations.

Stay Motivated and Consistent

Repaying student debt is a long-term process that requires patience and discipline. Celebrate small milestones whenever you pay off a portion of your loan. Staying focused on your financial goals and maintaining regular payments will gradually lead you toward financial freedom and peace of mind.